The concept of Islamic banking has gained significant popularity in recent years, with many individuals and institutions adopting it as an alternative to conventional financial systems. Islamic banking is based on the principles of Sharia law, which prohibits the payment or receipt of interest (riba) and promotes risk-sharing and profit-sharing arrangements.

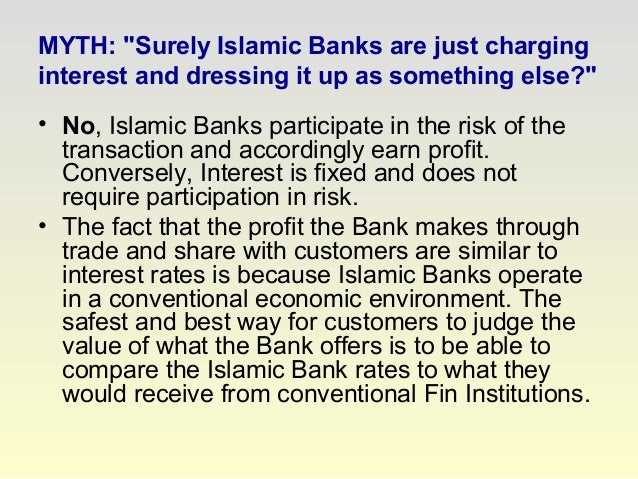

However, a closer examination of Islamic banking practices reveals several incongruities that challenge its claim to be truly Islamic. One of the main criticisms is the prevalence of interest-like transactions disguised as other forms, such as fees or profit rates. Critics argue that these transactions are in violation of the principles of riba and undermine the authenticity of Islamic banking.

Another issue revolves around the concept of risk-sharing. Islamic banking promotes the idea of sharing profits and losses between the bank and the customer. However, in practice, many Islamic banks have adopted risk-averse strategies that shift most of the risk onto the customer, while the bank still receives a fixed return. This contradicts the spirit of risk-sharing and raises questions about the true nature of Islamic banking.

Furthermore, the lack of uniformity in the interpretation and implementation of Sharia law across different Islamic countries and jurisdictions has led to discrepancies in the principles and practices of Islamic banking. This lack of standardization has created confusion and uncertainty, making it difficult to determine what truly constitutes Islamic banking.

In conclusion, while Islamic banking may have initially aimed to provide an alternative, ethical financial system based on the principles of Sharia law, its current practices and inconsistencies raise questions about its authenticity. The prevalence of interest-like transactions, the lack of true risk-sharing, and the lack of uniformity in its implementation all contribute to the argument that Islamic banking is not truly Islamic. To address these issues and restore the integrity of Islamic banking, there is a need for greater transparency, adherence to Sharia principles, and standardization in its practices.

Understanding Islamic Banking

Islamic banking is a financial system that operates in accordance with the principles of Shariah, or Islamic law. It is based on the idea of promoting economic well-being and social justice through ethical and responsible financial practices.

One of the main principles of Islamic banking is the prohibition of interest, or usury. This means that banks cannot charge or receive interest on loans or any other financial transaction. Instead, Islamic banks operate on a profit-sharing model, where both the bank and the customer share the risks and rewards of the investment.

Another principle of Islamic banking is the avoidance of investments in activities that are considered haram, or prohibited in Islam. This includes industries such as alcohol, gambling, pork, and interest-based financial institutions.

Islamic banking also encourages the concept of moral responsibility and fairness in financial dealings. It promotes transparency and accountability, and discourages speculation and excessive risk-taking.

To ensure compliance with Shariah principles, Islamic banks employ a dedicated board of Islamic scholars, known as the Shariah board. The board advises the bank on compliance with Islamic principles and reviews its operations to ensure they are in line with Shariah requirements.

Islamic banking offers a range of financial products and services, including savings accounts, investment accounts, personal and business financing, and trade finance. These products are structured in accordance with Islamic principles and are designed to meet the financial needs of individuals and businesses while adhering to the tenets of Islam.

- Savings accounts: Islamic banks offer savings accounts that provide a return on investment based on profit-sharing instead of interest.

- Investment accounts: Islamic banks offer investment accounts that allow customers to invest in Shariah-compliant investment opportunities.

- Financing: Islamic banks provide financing for personal and business needs through various Shariah-compliant financing options, such as Murabaha and Ijarah.

- Trade finance: Islamic banks offer trade finance services that facilitate international trade transactions in a Shariah-compliant manner.

Overall, Islamic banking aims to create a more equitable and ethical financial system that promotes economic stability and social welfare. It provides an alternative to conventional banking for Muslims who wish to conduct their financial affairs in accordance with their religious beliefs.

Problems with Islamic Banking

Despite its claims to be an ethical alternative to conventional banking, Islamic banking faces several challenges and criticisms. These problems stem from the inherent contradictions and ambiguities within Islamic finance principles.

- Lack of true risk-sharing: Islamic banking promotes the idea of risk-sharing between the bank and the customer. However, in practice, the burden of risk often falls on the customer alone, while the bank enjoys a guaranteed profit. This undermines the fundamental principle of fairness and equal sharing of risks and rewards.

- Complexity and lack of transparency: The principles and structures of Islamic finance can be complex and difficult to understand for both customers and regulators. This lack of transparency raises concerns about accountability and the potential for manipulation or exploitation by banks.

- Financial innovation and lack of standardization: Islamic finance lacks a standardized framework for products and transactions. This has led to a proliferation of complex financial instruments and structures that may deviate from the spirit of Islamic finance, such as the use of debt-based instruments disguised as Islamic contracts.

- Lack of global regulatory oversight: Unlike conventional banking, which is subject to international regulatory standards, Islamic banking lacks a unified global regulatory framework. This creates inconsistencies in practices and regulations between different countries and institutions, leading to potential loopholes and risks.

- Moral hazard: Islamic banking principles aim to promote ethical behavior and discourage speculation and excessive risk-taking. However, some critics argue that the absence of interest-based lending can lead to moral hazard, as it may incentivize borrowers to take on excess debt without proper consideration of risk.

- Challenges in integrating with the global financial system: Islamic banking faces difficulties in reconciling its principles with the existing global financial system. This includes issues related to accounting standards, tax treatments, and mechanisms for global money transfers.

- Insufficient Shariah compliance: Despite the existence of specialized Shariah boards to ensure compliance with Islamic principles, there have been instances of non-compliant practices and lack of proper oversight. This raises doubts about the credibility and authenticity of Islamic banking.

In conclusion, while Islamic banking may offer some advantages and attract a niche market, it is not without its problems. These challenges highlight the need for further refinement, standardization, and regulatory oversight to ensure that Islamic banking truly adheres to its ethical principles.

Examining the Prohibition of Interest

One of the fundamental principles of Islamic banking is the prohibition of interest, known as riba. This prohibition is derived from the Quran, which states that earning interest is a serious sin and is considered exploitative and unjust.

In Islamic banking, the concept of riba extends beyond just the charging of interest on loans. It also includes any unjust or exploitative gain from financial transactions. This means that all forms of interest, no matter how small or large, are strictly prohibited.

The prohibition of interest in Islamic banking is based on the principle that money itself has no intrinsic value and should not be able to generate more money without any effort or risk. Islamic banking operates on the principle of risk-sharing, where the lender and the borrower both share in the risk and reward of the investment or financing arrangement.

In contrast to conventional banking, Islamic banking focuses on profit and loss sharing (PLS) arrangements, such as mudarabah (profit-sharing) and musharakah (partnership). These forms of financing allow for a more equitable distribution of wealth and emphasize the ethical and social dimensions of banking.

Islamic banking also promotes the concept of ethical investment, where investments must comply with Shariah principles and avoid industries that are considered unethical, such as alcohol, gambling, and pork products.

To ensure compliance with Islamic principles, Islamic banks employ Shariah boards or supervisory committees, composed of Islamic scholars and experts in Islamic law. These boards review and approve financial products and services offered by Islamic banks to ensure they comply with Shariah principles.

Overall, the prohibition of interest in Islamic banking reflects the Islamic concept of justice, fairness, and socio-economic equality. By adhering to these principles, Islamic banking aims to create a more equitable and ethical financial system that benefits individuals and society as a whole.

The Role of Profit and Loss Sharing

One of the fundamental principles of Islamic banking is the concept of profit and loss sharing (PLS). PLS is considered a key feature of Islamic finance as it seeks to distribute the risks and rewards of investments between the bank and the depositor or investor. Unlike conventional banking, which operates on a fixed interest rate system, Islamic banks aim to generate profits by participating in the success and failure of their clients’ ventures.

In an Islamic banking system, PLS is implemented through various modes such as mudarabah (partnership), musharakah (joint venture), and wakalah (agency). These modes allow the bank and its clients to enter into partnerships where profits and losses are shared based on pre-agreed ratios or proportions.

Mudarabah is a type of partnership where one party provides the capital (the bank) and the other party provides the expertise or labor (the client). Any profits generated from the investment are shared between both parties according to the agreed-upon ratio, while losses are borne by the bank as the capital provider. This mode encourages the bank to carefully select investment opportunities and actively participate in the management of the venture.

Musharakah, on the other hand, involves a joint venture between the bank and the client, where both parties contribute capital and expertise. Profits and losses are shared based on a pre-determined ratio, and the bank’s role is not limited to passive financing but also includes active participation in the venture. This mode promotes a greater sense of partnership and risk sharing between the bank and its clients.

Wakalah is another mode of PLS, where the bank acts as an agent on behalf of the client to invest their funds. In this case, the bank is responsible for managing the investment and generating profits for the client. Any profits earned are shared between the bank and the client based on an agreed-upon ratio, while the bank bears the losses.

By implementing PLS, Islamic banking aims to create a more equitable and just financial system that aligns with the principles of Shariah (Islamic law). This approach encourages economic growth, fosters risk-taking, and promotes the fair distribution of wealth. However, it is important to note that the implementation of PLS in Islamic banking practices may vary among different countries and institutions, leading to some inconsistencies and challenges in achieving the desired objectives.

Questioning the Non-Riba Principle

The non-interest or non-riba principle is one of the fundamental principles on which Islamic banking is based. It prohibits the charging or paying of interest on loans, considering it as exploitative and unjust. While this principle is widely acclaimed by proponents of Islamic banking, there have been questions raised regarding its validity and effectiveness.

1. Interpretation and Implementation:

The non-riba principle is derived from Islamic texts such as the Qur’an and Hadith, which provide guidelines on financial transactions. However, the interpretation and implementation of these texts can vary among scholars and financial institutions. This has led to various interpretations of what constitutes riba, and thus, different practices among Islamic banks. The lack of consensus regarding the definition of riba raises concerns about the authenticity and effectiveness of the non-riba principle.

2. Alternative Forms of Riba:

While Islamic banks claim to operate on a non-riba basis, there are concerns about the existence of alternative forms of riba in their practices. For example, some Islamic banks engage in the practice of “mark-up” or “buy-back” transactions, where the bank purchases an asset and sells it back to the customer at a higher price with deferred payments. This can be seen as a disguised form of interest, as the customer is effectively paying more than the original price of the asset.

3. Competitiveness and Profitability:

The non-riba principle restricts Islamic banks from participating in conventional interest-based financial markets, which can limit their competitiveness and profitability. This is especially true in global financial markets where interest-based transactions are prevalent. Islamic banks may face challenges in attracting clients and generating profits due to their limited scope of financial activities. This raises questions about the sustainability and viability of Islamic banking in the long run.

4. Impact on Economic Growth:

Some critics argue that the non-riba principle can hinder economic growth in predominantly Muslim countries. By prohibiting interest-based transactions, Islamic banks may face difficulties in lending to businesses and individuals, reducing access to capital and impeding economic development. This calls into question the potential negative impact of the non-riba principle on overall economic growth.

Conclusion:

While the non-riba principle is a core tenet of Islamic banking, there are valid concerns and questions surrounding its interpretation, implementation, and impact. These issues highlight the need for ongoing dialogue, research, and reform within the Islamic banking industry to ensure its alignment with the principles it claims to uphold.

Challenges in Implementing Islamic Principles

Implementing Islamic principles in the context of banking poses several challenges that need to be addressed. The following are some of the main challenges:

- Interpretation of Islamic Principles: One of the key challenges in implementing Islamic principles in banking is the interpretation of these principles. Islamic principles can have different interpretations, and scholars may disagree on certain aspects. This can lead to confusion and inconsistency in the implementation of Islamic banking practices.

- Financial Innovation: Another challenge is the development of innovative financial products that comply with Islamic principles. Islamic banking aims to provide alternatives to conventional banking practices that are prohibited under Shariah law. However, developing new products that meet the requirements of Islamic principles can be complex and may require significant research and expertise.

- Lack of Standardization: The lack of standardization in Islamic banking practices is another challenge. Different countries and financial institutions may have their own interpretations and practices, which can lead to inconsistencies in the implementation of Islamic banking principles. Standardization is important to ensure transparency and trust in Islamic banking.

- Regulatory Framework: A robust regulatory framework is crucial for the implementation of Islamic banking principles. However, many countries still lack a comprehensive regulatory framework for Islamic banking. In some cases, Islamic banking operates under the same regulations as conventional banking, which may not be fully compatible with Islamic principles.

- Awareness and Education: The lack of awareness and understanding of Islamic banking principles among the general public is another challenge. Many people are still not familiar with the concept of Islamic banking and its underlying principles. Educating the public about Islamic banking and its advantages is essential for its successful implementation.

In conclusion, implementing Islamic principles in banking faces several challenges, including the interpretation of these principles, financial innovation, lack of standardization, regulatory framework, and awareness and education. Addressing these challenges is crucial for the effective and successful implementation of Islamic banking practices.

Contradictions in Islamic Banking Practices

Islamic banking, as a financial system rooted in Islamic principles, aims to create financial transactions that are compliant with Islamic law (Shariah). However, there exist several contradictions in the practices of Islamic banking that raise questions about their true adherence to Islamic principles.

- Interest-like Practices: While Islamic banking claims to be interest-free, it often employs alternative mechanisms such as profit-sharing agreements (Mudarabah) and cost-plus financing (Murabaha) that resemble conventional interest-based transactions. This raises concerns about the sincerity of Islamic banking in truly avoiding interest.

- Guaranteed Returns: Islamic banking products often guarantee returns to depositors, akin to conventional fixed deposit schemes. This contradicts the concept of profit and loss sharing (Musharakah), which is a fundamental principle in Islamic finance.

- Speculative Practices: Some Islamic banks engage in speculative activities that are considered haram (forbidden) in Islam. This includes investments in derivatives and complex financial instruments, which go against the principle of avoiding excessive uncertainty (Gharar).

- Sale of Debt: Islamic banks often engage in the sale of debt through the practice of securitization, where they package and sell debt contracts to investors. This contradicts the principle of avoiding debt-based transactions, as the sale of debt creates a debt-based instrument.

- Non-compliance with Shariah Standards: Many Islamic banks do not strictly adhere to Shariah standards and often rely on subjective interpretations, creating inconsistencies and widening the gap between theoretical principles and actual practices.

These contradictions in Islamic banking practices cast doubts on the claim of being truly Islamic. The need for a more comprehensive and consistent implementation of Islamic principles in financial transactions is crucial to ensure the integrity of Islamic banking.

Islamic Banks and Global Financial Markets

Islamic banks, despite their adherence to Islamic principles, have managed to become a significant player in global financial markets. Their unique approach to banking has allowed them to cater to a growing population of Muslims and non-Muslims alike who are seeking more ethical and responsible financial services.

Sharia-compliant financial products:

Islamic banks offer a range of financial products that comply with Sharia principles, such as Islamic bonds (sukuk), Islamic mortgages (ijara), and Islamic investment funds (mutual funds). These products are designed to be compatible with Islamic law, which prohibits the charging or receiving of interest (riba) and investing in industries that are considered unethical, such as alcohol, gambling, and pork-related businesses.

These Sharia-compliant products have gained popularity in global financial markets because they provide an alternative to conventional banking products that may conflict with individuals’ religious beliefs or ethical values. Islamic banks have successfully tapped into this demand, attracting not only Muslim customers but also non-Muslims who are looking for socially responsible and ethical investment options.

Increased market presence:

Islamic banks have expanded their operations beyond their traditional market in the Middle East and are now present in various countries around the world. This global reach has allowed them to access a wider pool of customers and tap into the growing demand for Sharia-compliant financial services.

Furthermore, Islamic banks have been able to forge partnerships and collaborate with conventional banks and financial institutions. These partnerships have enabled Islamic banks to access international markets, expand their range of products and services, and benefit from the expertise and infrastructure of larger financial institutions. This collaboration between Islamic banks and conventional banks has helped boost the visibility and acceptance of Islamic finance in global financial markets.

Financial stability and resilience:

Islamic banks have also demonstrated their resilience during global financial crises. The global financial crisis of 2008 highlighted the robustness of the Islamic banking system, as Islamic banks were relatively less affected compared to their conventional counterparts. This can be attributed to the Sharia principles that Islamic banks adhere to, which promote risk-sharing and discourage excessive speculation and debt accumulation. As a result, Islamic banks tend to have more conservative lending practices and stronger asset quality, making them more resistant to financial shocks.

Conclusion:

Islamic banks have emerged as a viable alternative in global financial markets, offering Sharia-compliant financial products and attracting a diverse range of customers. Their expansion and collaboration with the conventional banking sector have further enhanced their presence and acceptance in the global financial system. The resilience and stability demonstrated by Islamic banks during times of financial uncertainty have reinforced the trust placed in their ethical and responsible approach to finance.

Exploring the Role of Islamic Scholars

Islamic scholars play a crucial role in shaping the principles and practices of Islamic banking. Their expertise and knowledge in the field of Islamic jurisprudence (fiqh) enable them to provide guidance on the compatibility of financial products and transactions with Islamic principles.

One of the primary responsibilities of Islamic scholars is to issue fatwas (religious rulings) on various aspects of Islamic banking. These fatwas serve as a guide for bankers and customers in adhering to the principles of Islamic finance. Scholars analyze the nature and structure of financial products, assess their compliance with Islamic principles, and provide detailed guidance on their permissibility or prohibition.

Islamic scholars also play a role in ensuring transparency and ethical conduct within Islamic banking institutions. They are responsible for the supervision and monitoring of financial transactions to ensure that they comply with Shariah principles. Scholars may serve on Shariah boards or committees, which are responsible for approving and overseeing the operations of Islamic banks and financial institutions.

In addition to issuing fatwas and providing oversight, Islamic scholars also contribute to the development of Islamic financial products and regulations. They engage in research and scholarship to address emerging issues and challenges in Islamic finance. Their expertise helps in the continuous refinement and adaptation of Islamic banking practices to meet the needs of contemporary finance.

Furthermore, Islamic scholars act as educators and advocates for Islamic finance. They play a significant role in raising awareness among the public about the principles and benefits of Islamic banking. Scholars conduct seminars, lectures, and workshops to educate both Muslims and non-Muslims about the ethical and sustainable approach of Islamic finance.

The involvement of Islamic scholars in the field of Islamic banking is essential to maintain the integrity and authenticity of Islamic financial practices. They serve as guardians of Islamic principles and help ensure that Islamic banking remains true to its core values.

Impact on Economic Growth and Development

Islamic banking, despite its claimed adherence to Islamic principles, can have a significant impact on economic growth and development. While proponents argue that Islamic banking promotes ethical financial practices and social justice, there are several incongruities that undermine its potential benefits.

One key concern is the limited availability of Islamic banking products. In many countries, Islamic banking operates as a niche market with a limited range of products compared to conventional banking. This restricts the access of individuals and businesses to a diverse set of financial services, which can hinder economic growth.

Furthermore, Islamic banking faces challenges in terms of scalability and efficiency. Its adherence to religious principles imposes additional complexities and costs in relation to product development, compliance, and risk management. These challenges can deter potential investors and limit the ability of Islamic banks to expand their operations and contribute to economic development at a broader scale.

In addition, the lack of standardization in Shariah principles across jurisdictions poses a challenge to the growth of Islamic banking. The interpretation and application of Islamic laws vary among scholars and countries, leading to inconsistency in the development and implementation of financial products. This inconsistency can create confusion and uncertainty among market participants, inhibiting the growth and adoption of Islamic banking.

Another important point to consider is the impact of Islamic banking on financial inclusion. While Islamic banking promotes the idea of providing financial services to underserved populations, there is evidence suggesting that it may not effectively address the needs of the economically marginalized. The emphasis on asset-based financing and profit-sharing arrangements can limit access to credit for low-income individuals and small businesses, who often lack the necessary collateral or financial literacy to meet the requirements of Islamic financial products.

Moreover, Islamic banking faces challenges in integrating with the global financial system. The compatibility of Islamic financial instruments with conventional banking practices and regulations remains a subject of debate. The lack of harmonization between Islamic and conventional banking can create barriers to cross-border transactions and limit the ability of Islamic banks to tap into international markets, thereby hindering their potential contribution to global economic growth.

Overall, Islamic banking, despite its noble objectives, faces several incongruities that can impede its impact on economic growth and development. The limited availability of products, challenges in scalability and efficiency, lack of standardization, limitations in financial inclusion, and difficulties in integration with the global financial system are all factors that need to be addressed for Islamic banking to truly fulfill its potential as an ethical and inclusive alternative to conventional banking.

Comparing Islamic Banking to Conventional Banking

Islamic banking and conventional banking are two distinct models of financial systems. While conventional banking is based on interest and debt, Islamic banking follows the principles of Shariah law, which prohibits interest (riba) and promotes risk-sharing and ethical transactions.

1. Interest-free banking

Islamic banking operates on the principle of interest-free banking, which means that charging or receiving interest on loans is prohibited. In contrast, conventional banking relies heavily on interest as a primary source of income.

2. Profit and loss sharing

In Islamic banking, profits and losses are shared between the bank and the depositors or investors. This promotes a more equitable distribution of wealth and encourages the bank to engage in productive activities. In conventional banking, the bank bears all the risks and retains the profits, while the depositors receive a fixed rate of interest.

3. Ethical investments

Islamic banking strictly adheres to Shariah principles, which prohibit investments in industries deemed unethical, such as alcohol, gambling, or tobacco. In contrast, conventional banking has no such restrictions and can invest in any sector based on profitability.

4. Asset-backed financing

Islamic banking emphasizes asset-backed financing, where loans are provided based on the value of tangible assets rather than creditworthiness. This reduces the risk of default and prevents financing based on speculation. Conventional banking relies on creditworthiness and can provide loans based on a borrower’s credit rating.

5. Risk management

Islamic banking promotes risk-sharing between the bank and the customers, ensuring that both parties share the potential risks and rewards of a business venture. In conventional banking, risk management is primarily borne by the bank, while customers bear a minimal risk.

6. Regulation and governance

Islamic banking follows a strict set of guidelines and regulations based on Shariah law, ensuring ethical and transparent practices. Conventional banking is governed by various regulatory bodies and follows a regulatory framework based on economic principles.

7. Social responsibility

Islamic banking focuses on social responsibility and aims to benefit society as a whole. It promotes financial inclusion, charity, and community development projects. Conventional banking also engages in social responsibility initiatives but may prioritize profitability and shareholder returns.

| Islamic Banking | Conventional Banking |

|---|---|

| Based on Shariah principles | Based on economic principles |

| Interest-free banking | Relies on interest as a primary source of income |

| Profit and loss sharing | Fixed rate of interest for depositors |

| Invests in ethical industries | Can invest in any sector based on profitability |

| Asset-backed financing | Relies on creditworthiness for loans |

| Risk-sharing | Primarily bears the risk |

| Strict regulation based on Shariah law | Regulated by various bodies based on economic principles |

| Focuses on social responsibility | Engages in social responsibility initiatives to some extent |

In conclusion, Islamic banking and conventional banking differ in their principles, practices, and approaches to financial transactions. Islamic banking seeks to align financial activities with ethical and moral values, while conventional banking operates on economic principles.

Evaluating the Effectiveness of Religious Oversight

One of the key components of Islamic banking is the presence of religious oversight, which aims to ensure that the banking practices align with Islamic principles. However, it is important to evaluate the effectiveness of this oversight to determine whether it truly serves its purpose.

The Role of Religious Scholars

In Islamic banking, religious scholars play a crucial role in guiding and supervising the operations of financial institutions. These scholars are responsible for issuing fatwas (religious rulings) on various financial transactions to ensure their compliance with Shariah law.

Ensuring Compliance with Islamic Principles

The effectiveness of religious oversight can be evaluated based on its ability to ensure compliance with Islamic principles. This involves examining whether the banking practices adhere to the prohibitions on riba (interest), gharar (uncertainty), and haram (forbidden) activities. The role of religious scholars in issuing fatwas is essential in providing guidance on complex financial transactions and ensuring their conformity to Islamic principles.

Transparency and Accountability

Another aspect of evaluating religious oversight is the level of transparency and accountability within the Islamic banking system. It is important for religious scholars to have access to all relevant information and to conduct regular audits to ensure that the banks are operating in a transparent manner and are held accountable for their actions.

Adaptation to Changing Financial Landscape

The effectiveness of religious oversight can also be assessed based on its ability to adapt to the changing financial landscape. Islamic banking faces the challenge of keeping up with innovative financial products and practices, while adhering to Islamic principles. Religious scholars need to stay informed and updated on the latest developments in the financial industry to provide accurate rulings and guidance.

Challenges and Limitations

Despite efforts to ensure effective religious oversight, there are challenges and limitations that need to be addressed. These include differences in interpretation among religious scholars, the lack of standardized regulations across countries, and the potential for exploitation or fraudulent practices. Overcoming these challenges requires ongoing collaboration, research, and continuous improvement of religious oversight mechanisms.

Conclusion

Evaluating the effectiveness of religious oversight is crucial for the development and sustainability of Islamic banking. By ensuring compliance with Islamic principles, promoting transparency and accountability, and adapting to the changing financial landscape, religious oversight plays a vital role in maintaining the integrity of Islamic banking systems.

Case Studies of Failed Islamic Banking Institutions

In recent years, there have been several instances of Islamic banking institutions failing to adhere to Islamic principles and ultimately collapsing. These case studies shed light on the incongruities in Islamic banking practices:

-

The Bank of Al-Qard Al-Hasan:

This institution, based in Country X, claimed to offer interest-free loans to its customers in accordance with Islamic finance principles. However, it was discovered that the bank was engaging in unethical practices, including charging hidden fees and engaging in speculative investments. The bank eventually collapsed, leaving its customers with significant financial losses.

-

The Islamic Bank of Country Y:

This bank promoted itself as a fully Sharia-compliant financial institution, offering a range of Islamic banking products such as murabaha and ijara. However, investigations revealed that the bank was involved in lending practices that resembled conventional interest-based loans. It was discovered that the bank was charging excessive fees and engaging in usurious practices, contradicting the principles of Islamic finance. As a result, the bank faced a massive public backlash, leading to its eventual closure.

-

The International Islamic Banking Group:

This global Islamic banking group operated in multiple countries and marketed itself as a reputable institution adhering to Islamic principles. However, a detailed audit uncovered numerous discrepancies in its operations. It was found that the group had inflated its profit figures and engaged in speculative investments in violation of Islamic finance principles. This revelation caused a loss of trust and customer confidence, resulting in the eventual liquidation of the group.

These case studies demonstrate the challenges and shortcomings present in the implementation of Islamic banking principles. Despite claims of being Sharia-compliant, these institutions failed to uphold the ethical and financial standards required by Islamic finance. Such failures highlight the need for stronger regulations, transparent practices, and stricter oversight to ensure the integrity and success of Islamic banking institutions.

The Potential for Fraud and Corruption

One of the significant concerns surrounding Islamic banking is the potential for fraud and corruption. While Islamic principles emphasize ethical conduct and fairness, it is not immune to these risks.

The complexity of Islamic financial products and transactions makes it susceptible to fraudulent activities. The lack of standardized guidelines and regulations in many jurisdictions further exacerbates the issue. Unscrupulous individuals may exploit the gaps in the system and manipulate transactions to their advantage.

One example of potential fraud in Islamic banking is “Tawarruq” arrangements, where a customer buys a commodity using a loan and subsequently sells it to a third party to obtain cash. This practice has raised concerns about the misuse of the commodity trade and the potential for money laundering.

Corruption is another risk that Islamic banking faces. In some cases, bank officials may engage in corrupt practices such as bribery, embezzlement, or favoritism. These illicit activities undermine the integrity of the banking system and erode public trust in Islamic financial institutions.

To mitigate the potential for fraud and corruption, there is a need for robust regulatory frameworks and oversight mechanisms. Islamic banks should adhere to strict ethical guidelines, conduct thorough due diligence, and implement effective monitoring systems to detect and prevent fraudulent activities.

Furthermore, educating customers about the risks associated with Islamic banking and promoting transparency can help foster a culture of integrity. Implementing strong internal controls, whistleblower protections, and conducting regular audits is also vital in maintaining the credibility and trustworthiness of Islamic banking.

Efforts from regulatory bodies, financial institutions, and stakeholders are necessary to address the potential for fraud and corruption in Islamic banking and ensure its adherence to the principles of fairness and justice.

Taxation and Legal Issues in Islamic Banking

Islamic banking operates under a different framework compared to conventional banking, which gives rise to unique taxation and legal issues. These issues stem from the principles and practices followed by Islamic banks, which require adherence to Shariah law. In this section, we will explore some of the key taxation and legal issues faced by Islamic banks.

1. Shariah Compliance: One of the fundamental principles of Islamic banking is the requirement to comply with Shariah law. This means that Islamic banks must ensure that all their operations and transactions are in accordance with the teachings of Islam. From a taxation and legal perspective, this poses challenges as traditional tax laws and regulations may not align with Shariah principles. Islamic banks need to work closely with legal experts and tax authorities to find solutions that are both compliant with Shariah law and meet the requirements of the tax system.

2. Treatment of Interest: Conventional banks earn income through interest charged on loans and paid on deposits. However, interest is strictly prohibited in Islamic finance. Instead, Islamic banks operate on the basis of profit sharing and risk-sharing arrangements. From a taxation standpoint, this raises questions about how the income of Islamic banks should be classified and taxed. Some jurisdictions have developed special tax regimes for Islamic banks to address this issue, while others are still grappling with finding appropriate solutions.

3. Documentation and Legal Structures: Islamic banking transactions often involve complex structures and documentation to ensure compliance with Shariah law. For example, Islamic banks use contracts such as Murabaha, Musharaka, and Ijarah to achieve specific economic outcomes while adhering to Islamic principles. These unique legal structures may not fit neatly within the existing legal frameworks of some jurisdictions, leading to legal uncertainties and challenges. Islamic banks may need to work with legal experts and regulatory authorities to develop customized legal frameworks that accommodate the specific requirements of Islamic banking.

4. Tax Treatment of Islamic Financial Instruments: Islamic banks offer a range of financial products and instruments that have different characteristics compared to conventional financial products. These include Sukuk (Islamic bonds), Takaful (Islamic insurance), and Islamic mutual funds. From a taxation perspective, these instruments may be treated differently compared to their conventional counterparts. Tax authorities need to develop clear guidelines and regulations regarding the tax treatment of these Islamic financial instruments to ensure fairness and consistency in the tax system.

5. Cross-Border Transactions: Islamic banking is a global industry, with banks operating across different jurisdictions. This raises additional taxation and legal challenges, as different countries may have varying tax laws and regulations that may not be compatible with the principles of Islamic finance. Islamic banks need to navigate these cross-border complexities and ensure compliance with both Shariah laws and international tax regulations.

In conclusion, taxation and legal issues in Islamic banking are unique due to the adherence to Shariah law and the distinct principles followed by Islamic banks. Finding solutions that reconcile Islamic principles with existing tax laws and legal frameworks is an ongoing challenge for the industry. Close collaboration between Islamic banks, legal experts, tax authorities, and regulators is essential to address these issues and create a supportive environment for the growth of Islamic banking.

Examining the Lack of Standardization

One of the main critiques of Islamic banking is the lack of standardization in its practices. Unlike conventional banking, which operates under a unified set of international regulations, Islamic banking practices can vary significantly from one institution to another.

This lack of standardization poses several challenges. First, it makes it difficult for customers to compare and evaluate different Islamic banks and their products. This lack of transparency can be a barrier for potential customers who want to make informed decisions about their financial choices.

Moreover, the absence of standardization can lead to confusion and mistrust among customers. With different banks offering different interpretations of Islamic principles, there is a risk of inconsistency and contradiction, which can undermine the credibility of Islamic banking as a whole.

Furthermore, the lack of standardization makes it challenging to regulate and supervise Islamic banks effectively. Without a unified framework, regulators may struggle to monitor and enforce compliance with Islamic financial principles, which can compromise the stability and integrity of the banking system.

Efforts have been made to address the lack of standardization in Islamic banking. Organizations such as the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) have developed guidelines and standards to promote uniformity in financial reporting and auditing processes. However, these guidelines are not legally binding and are often adopted voluntarily, leading to variations in implementation.

In conclusion, the lack of standardization in Islamic banking poses significant challenges for both customers and regulators. Addressing this issue is crucial for the continued growth and development of Islamic banking as a viable alternative to conventional banking.

Consumer Perception of Islamic Banking

Consumer perception plays a significant role in shaping the success and growth of any industry, including Islamic banking. A positive perception of Islamic banking leads to increased trust and confidence among consumers, attracting them to use Islamic banking products and services. On the other hand, negative perceptions can hinder the growth and adoption of Islamic banking.

One of the key factors influencing consumer perception of Islamic banking is the understanding and knowledge of Islamic principles and practices. Many consumers may be unfamiliar with the concepts underlying Islamic finance, such as the prohibition of interest (riba) and the emphasis on ethical and socially responsible investing. Therefore, providing clear and accessible information about the principles and benefits of Islamic banking can help dispel misconceptions and enhance consumer perception.

Trustworthiness and transparency are essential characteristics that consumers look for in a banking institution. Islamic banks need to demonstrate these qualities to build and maintain consumer confidence. This can be achieved through ensuring compliance with Islamic principles, transparent disclosure of information, and ethical business practices. The credibility and reputation of Islamic banks in upholding Islamic values and principles can significantly influence consumer perception.

In addition, the availability and competitiveness of Islamic banking products and services also impact consumer perception. Islamic banks need to offer a wide range of products that cater to the diverse financial needs of consumers, ranging from personal banking to business financing. Moreover, these products should be competitive in terms of rates, fees, and customer service in order to attract and retain customers.

Furthermore, positive word-of-mouth and recommendations from existing customers can play a significant role in shaping consumer perception. Personal experiences and testimonials shared by satisfied customers can create a favorable image of Islamic banking and encourage others to consider using Islamic banks.

In conclusion, consumer perception of Islamic banking is influenced by various factors such as understanding of Islamic principles, trustworthiness, transparency, availability and competitiveness of products, and word-of-mouth recommendations. By addressing these factors and actively working to enhance consumer perception, Islamic banks can attract a larger customer base and foster the growth of the Islamic banking industry.

Addressing the Marketing of Islamic Banking

The marketing of Islamic banking plays a crucial role in attracting customers and creating awareness about its offerings. However, it is important to ensure that the marketing strategies align with the principles and values of Islamic banking.

Transparency and Honesty:

Marketing materials for Islamic banking should focus on providing clear and honest information about the products and services offered. Customers should be informed about the Shariah-compliant nature of the products, the specific rules and guidelines followed, and the benefits they can expect. This transparency helps build trust and credibility among potential customers.

Educational Approach:

Islamic banking is often misunderstood by the general public, so marketing efforts should aim to educate people about its principles and practices. This can be done through informative brochures, seminars, and online resources. By explaining how Islamic banking operates differently from conventional banking, potential customers can make more informed decisions and feel confident in choosing Islamic banking as their financial solution.

Emphasizing Ethical Values:

One of the key selling points of Islamic banking is its adherence to ethical principles. Marketing materials should highlight the ethical values that Islamic banking promotes, such as social responsibility, fairness, and justice. By emphasizing these values, Islamic banks can differentiate themselves from conventional banks and appeal to customers who prioritize ethical considerations in their financial decisions.

Personalized Customer Service:

Islamic banking is known for its emphasis on a more personal and customer-centric approach. Marketing efforts should highlight this aspect and emphasize the availability of dedicated relationship managers, who can provide tailored financial solutions. By showcasing the personalized customer service offered, Islamic banks can attract customers who value a more individualized experience.

Collaboration with Islamic Scholars:

In order to ensure that marketing materials accurately portray the Islamic banking principles, it is important for banks to collaborate with reputable Islamic scholars. These scholars can review and endorse the marketing content, ensuring it aligns with the Shariah guidelines. This collaboration adds an extra layer of credibility and authenticity to the marketing efforts.

Building Trust through Customer Testimonials:

Customer testimonials can be a powerful marketing tool for Islamic banks. By featuring testimonials from satisfied customers who have benefited from Islamic banking products and services, potential customers can gain confidence in the offerings. These testimonials can highlight the positive impact Islamic banking has had on customers’ financial lives, further promoting trust and credibility.

Overall, the marketing of Islamic banking should focus on transparency, education, ethical values, personalized customer service, collaboration with scholars, and building trust through customer testimonials. By following these principles, Islamic banks can effectively attract and retain customers who align with their values and principles.

FAQ

What is Islamic Banking?

Islamic banking refers to a financial system that operates according to the principles of Islamic law, known as Shariah. It prohibits the charging or payment of interest and promotes risk-sharing and ethical investment.

Why is Islamic banking considered as not Islamic?

Islamic banking is considered not entirely Islamic due to several incongruities that exist within the industry. Critics argue that some practices, such as the use of interest-based benchmarks and the lack of full transparency, are not in line with Shariah principles.

Can you give examples of incongruities in Islamic banking?

One example of incongruity in Islamic banking is the use of interest-based benchmarks, such as LIBOR, to set the profit rates on certain products. This goes against the Islamic prohibition of charging or paying interest. Another example is the lack of full transparency in some Islamic banks, making it difficult for customers to fully understand the nature of their transactions.

What are the criticisms of Islamic banking?

Critics of Islamic banking point out several shortcomings in the industry. They argue that some banks claim to be Shariah-compliant without adhering to all the necessary principles. Additionally, they highlight the lack of standardized regulations and oversight, which can lead to inconsistencies and potential misuse of funds.